The AI Ecosystem Map: How Major Platforms Work Together and Apart

Five AI ecosystems dominate 2026. Learn how OpenAI, Anthropic, Google, Meta, and Microsoft compete, converge, and what it means for your business.

There’s a conversation happening in AI right now that most business owners aren’t part of. Not because they don’t care. Not because they can’t follow the technical details. They’re not part of it because the conversation is happening at the infrastructure level, inside protocol committees and open-source governance bodies and foundation model boardrooms, and nobody is bothering to translate it into language that matters for the people who’ll feel the consequences most.

That conversation is about ecosystems. Not individual tools. Not which chatbot gives better answers on a Tuesday afternoon. The real question shaping the next decade of business technology is simpler and bigger than that: who controls the platforms, how do they connect, and what happens to your business when the ground shifts underneath the tools you depend on?

I’ve been mapping this territory for months. Partly for my own understanding, partly because clients keep asking me the same question in different words: “Should I be worried I’m building on the wrong platform?”

Depends on what you know about the landscape. So let’s build that knowledge together. Not a feature comparison chart (those go stale within weeks), but a structural overview of how these AI ecosystems for business operate, compete, and in some surprising cases, actively help each other.

The Five AI Ecosystems That Matter Right Now

As of mid-2026, five major ecosystems dominate the AI landscape. Each is anchored by a foundation model and surrounded by an expanding constellation of tools, platforms, and integrations. They’re not interchangeable. Each has a center of gravity that pulls users toward a particular way of working, and understanding those gravitational forces is what separates a good AI investment from a frustrating one.

OpenAI: The Consumer Gateway

OpenAI is still the name most people think of when they hear “AI.” And the numbers explain why. ChatGPT hit 900 million people using it every week by February 2026. By May, it crossed one billion monthly active app users, according to Sensor Tower estimates that Reuters picked up in June. That makes it the fastest app in history to reach that milestone. Faster than TikTok, faster than Instagram, faster than Google Maps.

The ecosystem centers on ChatGPT as the primary interface. GPT models power everything from the consumer chat product to enterprise APIs to the Codex coding agents. OpenAI wants to be the front door, the first place you go when you think “I need AI for this.” The integration of apps, plugins, and custom GPTs inside ChatGPT creates a self-contained world where you can search the web, analyze data, generate images with DALL-E, and interact with third-party services without ever leaving the chat window.

The revenue growth is staggering. OpenAI’s CFO Sarah Friar confirmed the company crossed $20 billion in annualized revenue for 2025. By March 2026, Reuters reported that number had jumped past $25 billion, roughly $2 billion every month. On March 31, SoftBank co-led a $122 billion funding round that valued the company at $852 billion. Then, on June 8, OpenAI filed a confidential S-1 with the SEC. Two days ago. The formal path to what could become one of the largest IPOs ever recorded just started.

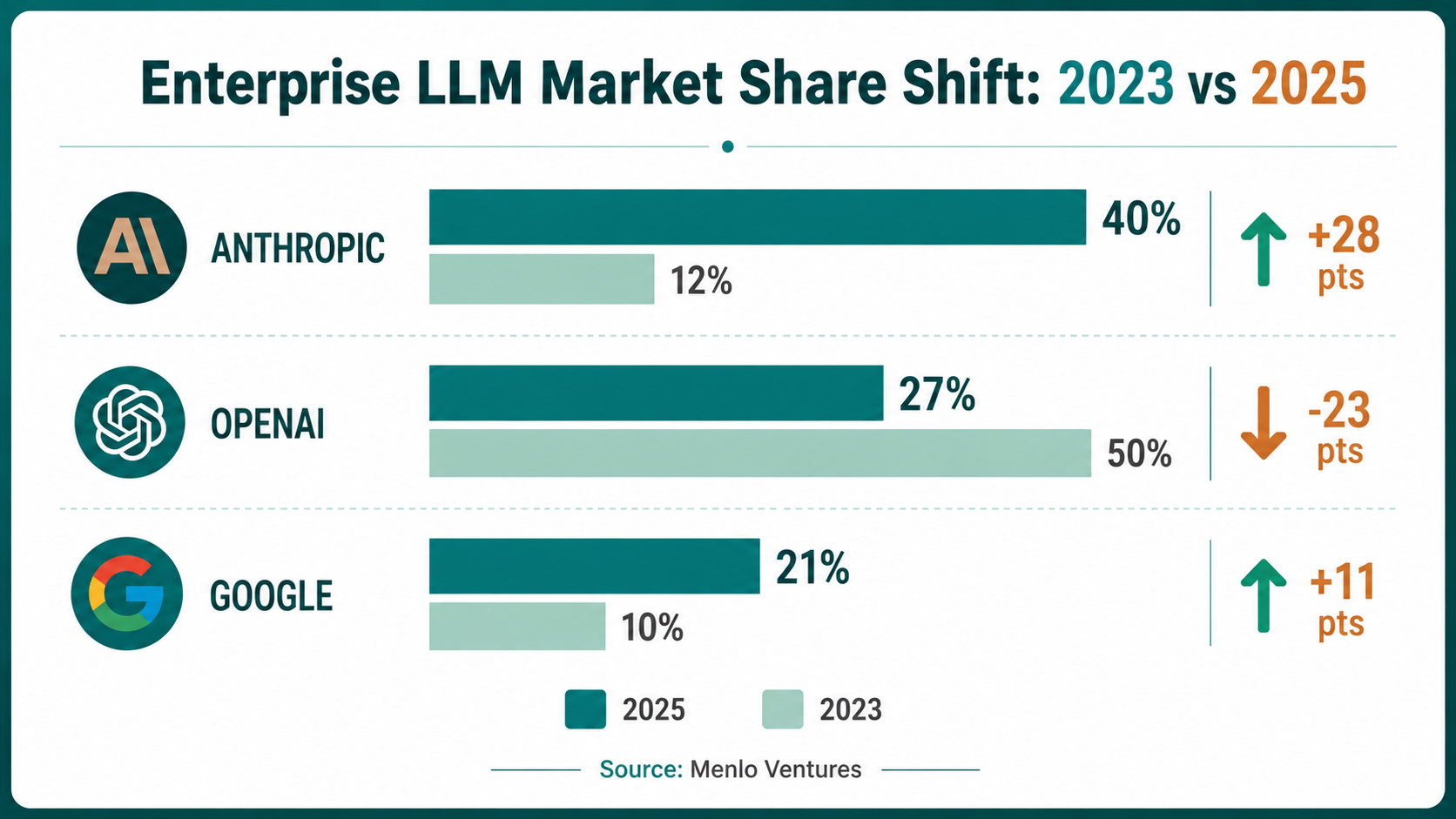

But here’s where it gets complicated. OpenAI’s grip on the enterprise market is loosening, and the data is hard to argue with. Menlo Ventures has been tracking this shift since 2023, when OpenAI controlled half of all enterprise LLM spending. Half. Two years later, that number sits at 27%. And it’s not just enterprise buyers moving. Apptopia reported in May that ChatGPT’s U.S. mobile app share dropped below 40% for the first time. Consumers still love it. The people writing the checks? They’re shopping around.

There’s a cautionary story here too. OpenAI killed Sora, its AI video product, in March 2026. I followed this one closely. Forbes and Appfigures reported that Sora was burning roughly $15 million a day in inference costs while generating $2.1 million in total lifetime revenue. Total. Not per day. The $1 billion Disney licensing partnership that was supposed to anchor the business fell apart alongside it. Even the most well-funded AI company in history can’t sustain every product line. That’s worth remembering when you’re betting your business processes on a specific tool.

Anthropic: The Enterprise and Developer Favorite

I’ve been watching Anthropic for a while now, and what happened with their revenue in 2026 caught even me off guard. At the end of 2025, their annualized run-rate sat at about $9 billion. Two months later it had nearly doubled to $14 billion. Then it went vertical. April: $30 billion. May: $47 billion. VentureBeat covered it. Simon Willison charted it. Dario Amodei, their CEO, told reporters the growth outstripped their own internal forecasts by a factor of eight. I don’t think I’ve ever seen a revenue curve like that in enterprise software.

The Menlo Ventures report from December 2025 put Anthropic at 40% of enterprise LLM API market share, up from 12% two years earlier. OpenAI went from 50% to 27% over that same period. Claude Code, their developer tool, is a big part of why. Developers I talk to treat it the way an earlier generation treated Stack Overflow, as something they open every morning and close when they’re done for the day. By February 2026 it was pulling in $2.5 billion in run-rate revenue on its own.

Anthropic raised a $30 billion Series G at a $380 billion valuation in February. Reuters reported in April that the company was weighing a new round above $900 billion. And on June 1, Anthropic filed its own confidential S-1 for an IPO. Think about that for a second. Two companies worth a combined $1.8 trillion, both preparing to go public in the same week. That’s the kind of moment that marks a turning point.

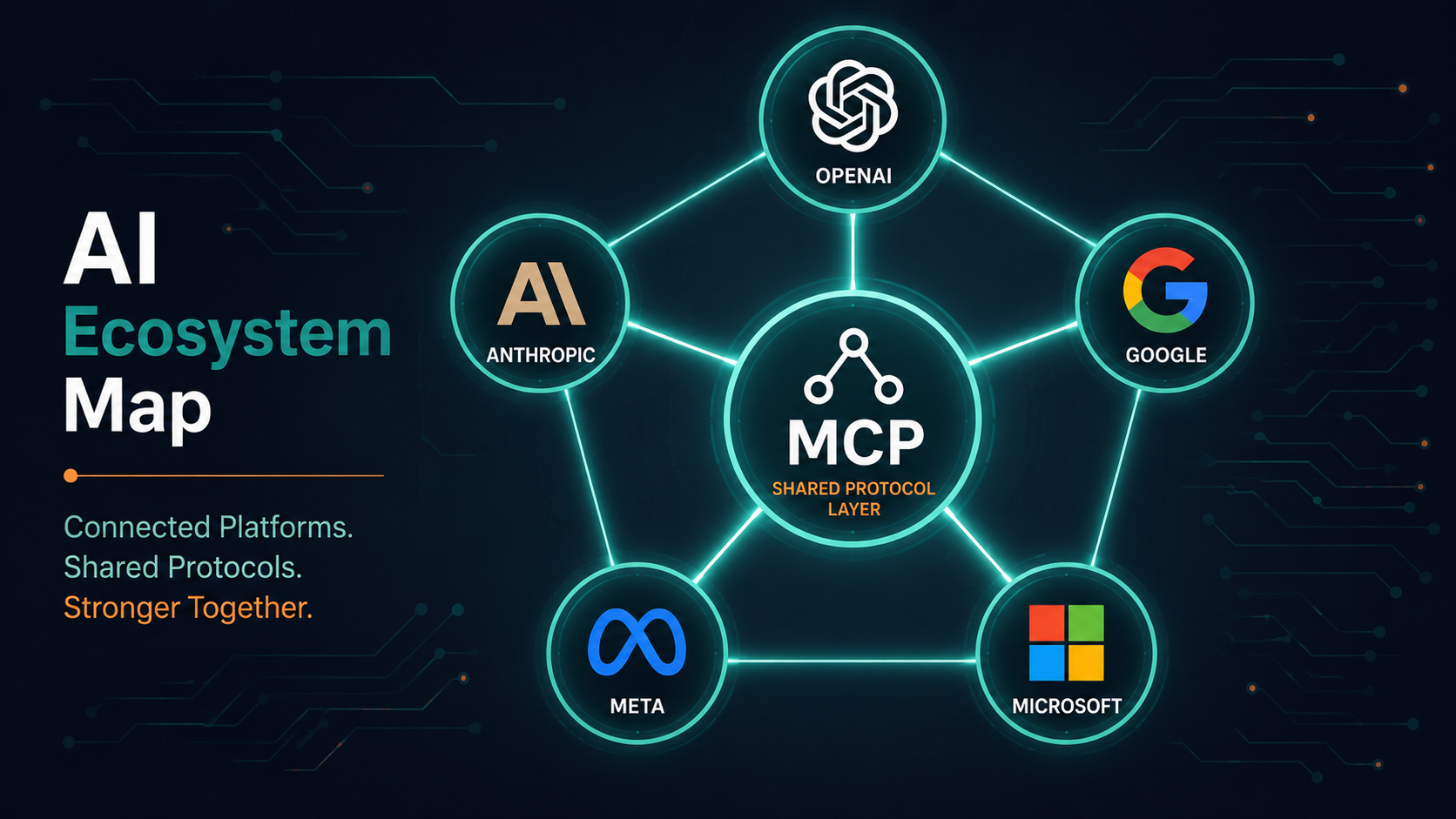

But the thing from Anthropic that might matter most for your business isn’t a model. It’s the Model Context Protocol, or MCP. Think of it as a universal adapter that lets AI models connect to external tools, databases, and APIs in a standardized way. Anthropic built it, then gave it away to the Linux Foundation’s Agentic AI Foundation. By making MCP an open standard instead of keeping it proprietary, Anthropic positioned itself as the connective tissue of the whole AI agent economy. OpenAI adopted it. Google adopted it. Microsoft adopted it. As of December 2025, there were over 10,000 active public MCP servers and the SDK was being downloaded 97 million times a month across Python and TypeScript. People call it the “USB-C for AI.” That comparison holds up.

One more thing worth knowing. Claude is now available across all three major cloud platforms: AWS Bedrock, Google Cloud Vertex AI, and Microsoft Azure Foundry. No other frontier model can say that. If OpenAI owns the consumer front door, Anthropic is building the plumbing that connects everything behind it.

Google: The Full-Stack AI Ecosystem

Google’s AI ecosystem is the broadest and deepest, and that’s both its greatest strength and its biggest source of confusion for people trying to understand it. Gemini models power consumer search, the Gemini app, Google Workspace integrations, the Vertex AI developer platform, and the cloud infrastructure that other AI companies rent. The Gemini app alone had 750 million monthly active users by early 2026. Analysts at Tech Insider predicted it would pass one billion by Q3.

What makes Google different from everyone else on this list is vertical integration. They design their own AI chips. At Google I/O 2026 in May, they unveiled the eighth generation: TPU 8t for training, TPU 8i for inference. They run their own cloud. They build their own models. They distribute through products that billions of people already use every day. And here’s the part that makes the competitive dynamics genuinely strange: Anthropic buys Google’s TPUs. Meta has negotiated for Google TPU access. Google is selling picks and shovels to the people mining the same gold.

It gets even more intertwined. Reuters reported in April 2026 that Google is investing up to $40 billion in Anthropic, while simultaneously hosting Claude models on Vertex AI and competing against Claude with Gemini. At I/O 2026, Sundar Pichai called this the beginning of the “agentic Gemini era,” where AI doesn’t just answer questions but acts as a supervised assistant that can plan, reason, and take action across Google’s product suite. Google also contributed its Agent-to-Agent protocol to the open standards effort and launched enterprise MCP servers.

The ecosystem stretches from consumer products (Search, Gmail, Docs) through developer tools (Vertex AI, Gemini API) to raw infrastructure (TPUs, Cloud). That’s a stack no single competitor can match.

30+ years of research strategy on projects for Oracle, Cisco, PayPal, and Walmart — now helping small businesses adopt AI that actually delivers.

More about George →Keep reading

Kimi K3 arrived at a third of Fable 5’s price with near-matching benchmarks. Here’s what the AI pricing collision means for small business owners and what to watch next.

Small business owners are deploying AI agents across four key roles. The ones getting results treat it with hiring discipline, not as a coworker. Practical guide from Galyx.

A practitioner’s guide to Perplexity AI for small business research. What it does, how to use it, and where it fits in your AI workflow.